How to Automate Your Finances With a Money Flow System

If the word “budget” makes you curl into a ball or run in the other direction, you’re not alone. I get it. Budgeting might conjure images of tedious number-crunching and snooze-inducing spreadsheets.

And if you’re like me, you don’t really enjoy having to pay meticulous attention to your finances. If the 50-30-20 budget, zero-sum budget, or standard budget where you assign dollar amounts to specific spending categories just don’t work for you, consider creating a money flow system instead.

A money flow system is a budgeting method where you use different bank accounts for spending and saving, where money flows - often automatically - between accounts and out toward expenses and bills.

A major benefit of such a system is that you’re not tracking every single transaction. Money flows down from a central account into designated accounts you can use for specific categories. As long as you don't outspend the amount available in the account, you're on budget. You can think of it as a series of rivers flowing to and from larger lakes.

I started doing this about a decade ago, and it’s pretty much a well-oiled machine. Through such a system, I’m able to manage my monthly expenses, tuck away money for savings, and avoid having to stress about my money on a daily basis. Here’s how to go about creating your own money flow system:

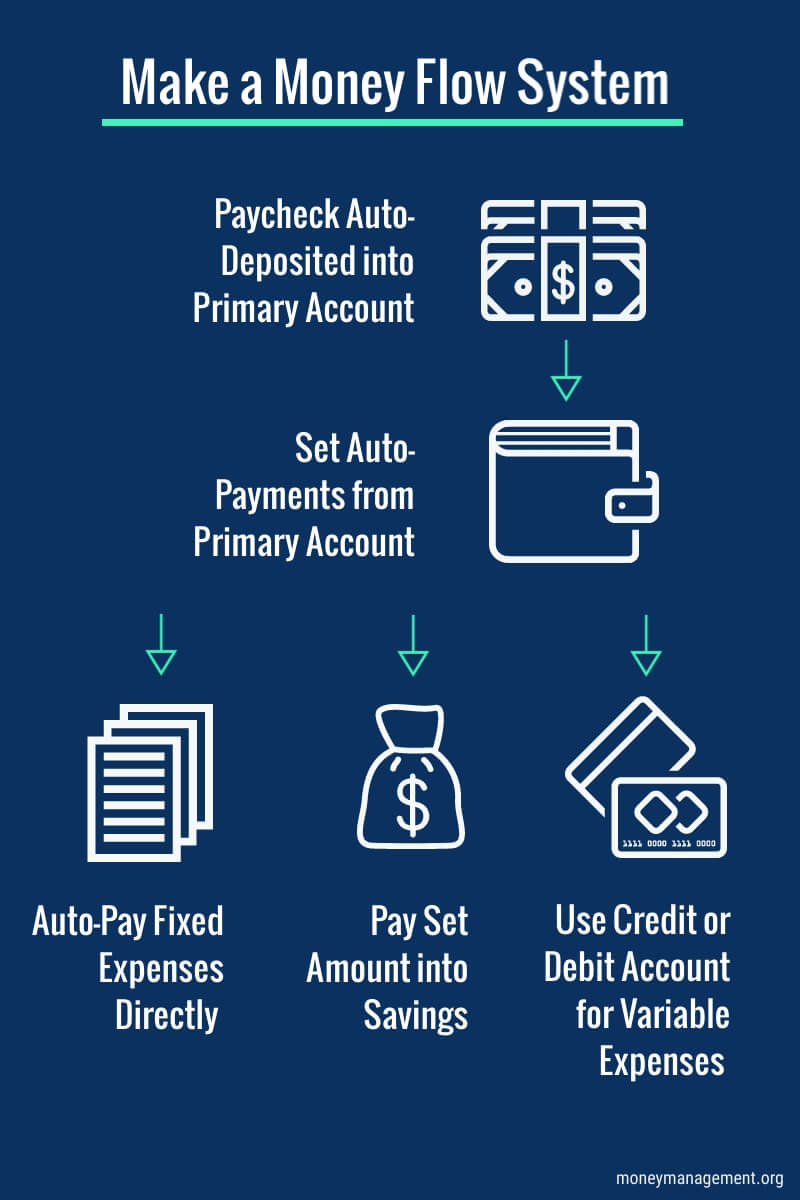

Step 1: Set Up Different Bank Accounts

To keep things simple, consider having four accounts. The first bank account, or Bank Account A, is considered your Main Account or your “hub.” This is where your paychecks get deposited, and where you pull funds from to pay your bills.

The second account is for your savings. Think emergency fund, vacation fund, funds for back-to-school or holiday shopping, or perhaps to buy a house or car. This second bank account, which can also be called Bank Account B or your Savings Account, can be broken down into several smaller accounts (if that helps).

Account C is for your retirement. This might be an employer-sponsored retirement plan, such as a 401(k) or 403(b); or a separate account for an IRA, solo 401(k) or SEP IRA. You might have another account for taxable investment accounts, such as micro-investing apps and stock brokerage platforms.

Your final account should be a debit account or a credit card (presuming you can trust yourself to not outspend your monthly limit). The idea is to have an account to use for variable expenses. You don't have to track individual purchases, but you do have to stay within the maximum allowance for that account.

As someone who thrives by systems, my money flow is far more complicated than it needs to be. I have about seven different accounts for my spending, saving, and investing needs. One is just for variable, or discretionary expenses, and several are for savings, retirement, and investments. Feel free to keep your system as simple or as complicated as suits your needs.

Step 2: Designate Payments to Your Accounts

Next, list all your bills and the payment due dates. Then put an arrow from each bill to the account the money will come out of. For most, it’ll be from Account A, or your main bank account.

To stay on top of payments, reach out to each company and see if they’re open to moving payment due dates on your bills so they’re more in sync with your cash flow.

You might put some payments on your credit card. For instance, health insurance premiums, cell phone payments, and utility bills. Besides racking up credit card reward points, it might come in handy when your bills don’t sync up with your payments. If you do so, just make sure you pay the balance in full each month.

Step 3: Automate Deposits into Savings

After you’ve devised a flow for all your bills, you’ll then want to figure out the flow from your main bank account to your different savings accounts. For instance, you might autosave $100 a month from your main account to your emergency fund, $200 toward your next vacation, and $200 into your IRA account.

Of course, the amounts and when you push money into one of your savings accounts depends on when you get paid, and what works best for you. I autosave once a month, but some people might feel more comfortable auto-saving less frequently.

Step 4: Make Tweaks As Necessary

Making adjustments along the way is a part of any spending plan. When you create a money flow system, you might want to change the amounts you’re saving, or shift accounts around. And if you run into any snags, such as putting too much on your credit card, you might want to consider paying your bills or buying groceries from your main account.

Once you set up a money flow system, it will be easier to make minor changes and tweaks as needed. If you’ve just set it up, it’s particularly important to check in on it every month or so.

If you would like help coming up with a spending plan, reach out to the NFCC-certified financial counselors at MMI. We can help you create a budget that suits your needs and your goals.